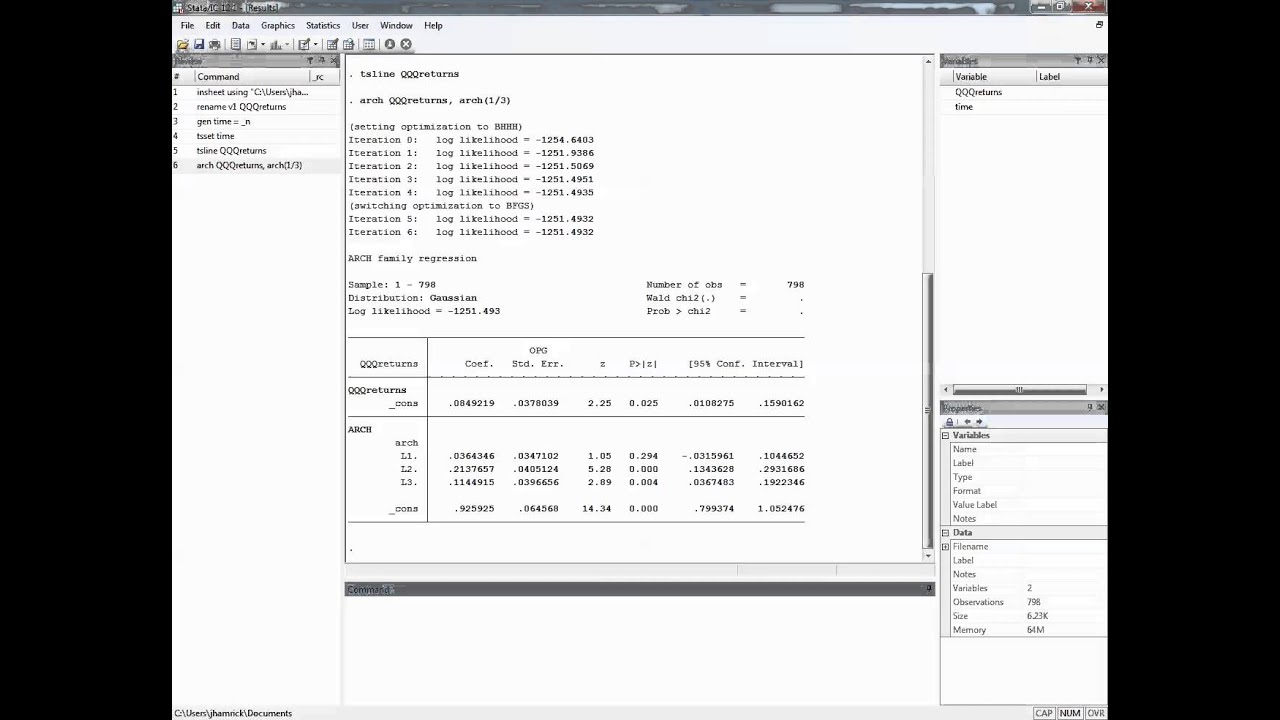

Using the ARCH LM Test in Stata to Investigate the Appropriate Order of an ARCH Specification Jeff Hamrick 7:06 11 years ago 32 117 Скачать Далее

(EViews10): How to Estimate Standard GARCH Models #garch #arch #volatility #clustering #archlm CrunchEconometrix 14:25 4 years ago 52 824 Скачать Далее

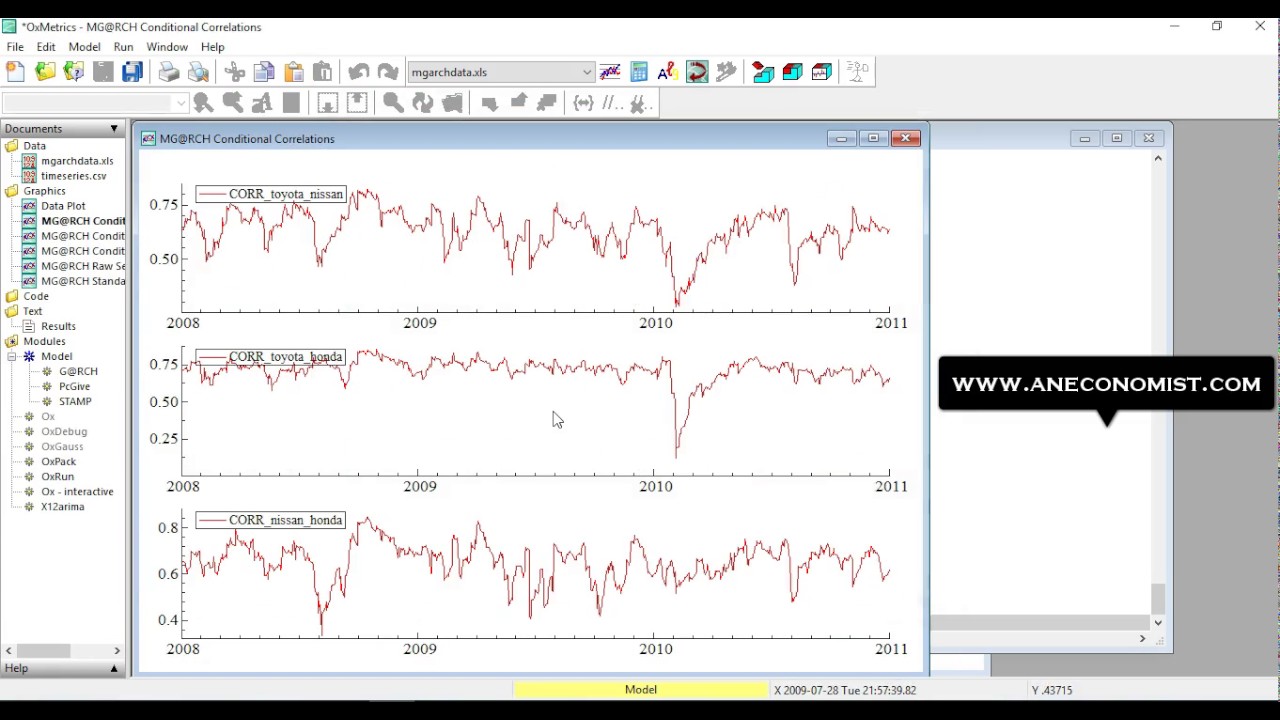

Multivariate GARCH DCC Estimation AnEc Center for Econometrics Research 2:23 7 years ago 30 279 Скачать Далее

(EViews10): How to Estimate GARCH-in-Mean Models #garchmodels #garchm #tgarch #volatility #egarch CrunchEconometrix 7:52 4 years ago 12 345 Скачать Далее